Every year the number of Russian citizens who decide to insure their lives is increasing.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem , contact a consultant:

+7 (499) 938-81-90 (Moscow)

+7 (812) 467-32-77 (Saint Petersburg)

8 (800) 301-79-36 (Regions)

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FREE !

This is due to the fact that among the population the level of responsibility for their relatives and friends, who may find themselves in a difficult financial situation after the loss of a breadwinner, is rapidly growing.

A timely issued insurance policy will help the family of the insured person resolve all financial issues that may result from his death.

Legal regulation

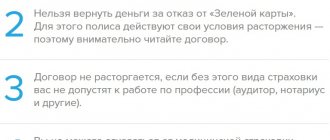

Article 958 of the Civil Code of the Russian Federation establishes a provision according to which a citizen has the right to return part of the funds paid towards the registration of a compulsory motor liability insurance policy if the insurance risk and the possibility of an insured event becoming unrealistic for a reason unrelated to the insured event itself. The amount of payment is determined in proportion to the remaining insurance period.

In other words, this means that it is impossible for a citizen to receive an insurance payment for reasons unrelated to the occurrence of an insured event. Since the only basis for providing compensation under compulsory motor liability insurance is the fact of a registered road accident, the circumstances that occur should not be related to the accident. For example, when a legal entity (insurer) was liquidated, or when a car was completely destroyed due to other circumstances (fire).

However, if the termination of rights to the insured property was associated with the direct actions of a citizen (when selling a car), this provision does not apply.

The norm in question also provides for the possibility of unilateral termination of the contract without explanation at the initiative of the policyholder. But in this case, no payments or compensation are provided, unless otherwise provided by the insurance contract. As a general rule, termination of a contract at the initiative of the insurance company is not allowed.

The considered rules are general and apply unless other rules are established by specialized regulatory legal acts regulating a particular area of insurance, which will be discussed below.

Legal regulation of termination of a life insurance contract

There is no regulatory act regulating the return of funds upon early repayment of a mortgage. This situation is regulated by Chapter 958 of the Civil Code of the Russian Federation and other federal laws (such as the Law “On the Protection of Consumer Rights”), as well as general insurance regulations.

Banks, in their own interests, refer in this case to clause 3 of Art. 958 of the Civil Code of the Russian Federation. In accordance with it, the insurance premium paid to the company is non-refundable, unless otherwise specified in the insurance contract.

Borrowers can rely on Article 16 of the Law of the Russian Federation “On the Protection of Consumer Rights” in the latest edition, according to which:

- if the consumer has losses as a result of the execution of the contract, then such losses are subject to compensation by the bank in full;

- damages caused to the consumer as a result of violation of his right to free choice of goods and services are compensated. According to the law, banks cannot provide services that require the use of other services that the consumer does not need.

Cooling period

This term was used and introduced by Bank of Russia Decree No. 3854. The prerequisite for this was a large number of dissatisfied complaints from citizens regarding the forced inclusion of additional services as basic ones when issuing an MTPL insurance policy.

The period should be understood as a five-day period from the moment of concluding an agreement with the insurer, during which a citizen has the right to terminate the agreement, losing a minimum percentage of the total cost of the insurance policy, or returning the money in full. It is important that no grounds for insurance payment arise during this period.

ATTENTION !!! According to the provisions of the instruction, the amount paid for the insurance policy must be returned in full if the citizen applied within 5 days from the date of conclusion of the contract, but the insurance period has not yet begun.

If termination of the contract occurred during the period (5 days from the start of the insurance period), then the insurer has the right to withhold a certain amount of money proportional to the number of days that have passed.

The five-day period established by law is the minimum and can be increased based on the agreement between the insurer and the policyholder. Such rules must be recorded in writing.

IMPORTANT !!! The policyholder's application requesting termination of the contract within the specified period must be considered within 10 working days.

The law establishes an exhaustive list of types of insurance to which these rules apply. This includes not only OSAGO, but also CASCO.

If the period established by law/contract has not yet expired, for a return you should write an application in simple free written form and submit it to the organization. The list of documents is not established in the law, so you need to proceed from the provisions of the concluded agreement. If any information about this is missing, one application will be sufficient; if the contract specifies specific documents, they should be attached to the application.

Termination of a life insurance contract

The legislation in force on the territory of the Russian Federation (Article 958 of the Civil Code) allows citizens taking part in the life insurance procedure to terminate the contract with their insurer.

If there is an urgent need to terminate the contract, the insured person must take into account the existing nuances, thanks to which it will be possible to significantly reduce financial losses.

Currently, there are three ways in which the parties can terminate a life insurance contract:

- if the insured person violates the terms of payment of insurance premiums, as well as other terms of the contract;

- at the request of the insured person;

- when the client transmits knowingly false data to the insurance company necessary for drawing up a contract.

Federal legislation of the Russian Federation allows for early termination of life insurance contracts if the following factors are present:

- if the insured person has an accident that was not specified in the contract as an insurance risk;

- if the insured person’s circumstances have changed and nothing will threaten his life and health in the coming years.

In the event that the insurance contract was terminated due to an insured event not covered by this document, the insurer has the opportunity to use the premium (when calculating it, the actual validity period of the contract is taken into account).

The insured person who initiated the termination of the relationship with the insurer will not be returned the redemption amount deposited to the cash desk as an insurance premium (or to the current account) of the insurance company.

Each person, when deciding to participate in the voluntary life insurance procedure, must first familiarize himself with all the offers of the insurance company.

After the insurer accepts the application to terminate the contract, under Art. 452 of the Civil Code of the Russian Federation, an agreement to terminate the contract must be signed in writing.

Currently, Russian citizens are offered several types of insurance contracts, the difference of which lies in the conditions, risks and methods of payment of insurance amounts.

A very important point in this process is the correct choice of the company with which the life insurance contract will be concluded.

To avoid possible troubles in the future, you should cooperate only with trusted insurers who have been in the insurance market for many years and have a positive reputation.

Find out what the social insurance financial system is in the article: social insurance system. You can find out what the rules of health insurance are here.

You can read about the mortgage insurance agreement at this link.

Grounds for termination of an insurance contract

If the cooling-off period has ended, the contract can be terminated on the grounds provided for by a special law or other regulatory legal act.

In the case of compulsory motor liability insurance, early termination of the contract is permitted in the following cases:

- death of the owner or another person with whom the insurance contract was concluded;

- complete destruction of the car for a reason unrelated to the accident;

- liquidation of a legal entity, expiration of a license, or other circumstances related to the inability of the insurer to fulfill the terms of the contract.

In the event of the death of the policyholder, the interested party (usually a relative) must collect all documents related to the MTPL insurance policy, as well as a copy of the death certificate and provide all this to the insurer's office. No additional actions are required, the return takes place on the basis of an agreement.

If the car is completely destroyed, the policyholder also has the right to apply to terminate the contract as it no longer serves any purpose. To receive payment, you must provide a document confirming the fact of loss of property for certain reasons. This rule also applies when disposing of a car within the framework of government programs.

Upon liquidation of a legal entity, or in the event of revocation of the insurer's license, the citizen has the right to terminate the contract and receive his money back. However, in practice this is very problematic, since in most cases the company goes bankrupt.

IMPORTANT !!! A change of owner (sale, donation, or other basis) may also become a reason for termination of the concluded contract. For the new car owner, the old contract has no meaning and its use is impossible (only if the insurance policy is not open).

The old owner will also not be able to use this policy, however, if there is a significant period of time left before the end of the term, it is possible to terminate the contract in order to receive most of the money.

Termination of the contract at the initiative of the insurer is possible if it is discovered that a citizen has provided false information in order to issue an insurance policy. In certain circumstances, this may result in additional legal liability. On this basis, a citizen cannot count on receiving funds as a result of a terminated contract.

Consequences of termination of a life insurance contract

If a life insurance contract is terminated early, the consequences will be as follows:

- the previously insured person ceases to be such and in the event of an insured event provided for by the terminated contract, he loses the right to payment of insurance compensation by the insurer

- the person may receive a full or partial refund of the insurance premium

- the insurance premium may not be returned to the person, since the contract provided for the corresponding condition

Thus, with the termination of the contract, all mutual rights and obligations of the parties cease, with the exception of certain rights and obligations, if this is provided for by the contract or law.

Procedure or how to get money back for insurance

Depending on the specific circumstances, as well as the grounds for termination of the contract, the return procedure may vary.

First you need to prepare documents, which can be:

- a concluded contract with an insurance company, as well as a check received after payment;

- identification document of the applicant;

- a document confirming the transfer of ownership of the car;

- a copy of the death certificate;

- other documents confirming the basis for early termination of the contract.

Some additional conditions may be established by the insurer itself; these provisions must not contradict current legislation and are also subject to mandatory inclusion in the contract.

IMPORTANT !!! To find out as accurately as possible about the termination procedure, you should study your contract. You can also contact the organization’s employees and ask them this question.

Depending on the situation, you can count on receiving funds:

- the policyholder himself who entered into the contract;

- a representative or other person who has entered into an insurance contract;

- relatives of the deceased or declared incompetent insured.

An application requesting termination of the contract and refund of funds must be considered no later than 10 days from the date of application and provision of all necessary documents.

Insurers who provide services for issuing electronic policies (alfa insurance online, SOGAZ, RESO and others) can carry out the entire procedure for returning funds through a special form on their website. To do this, you should study the conditions of your own insurance company.

The amount of money is determined based on the number of days that have passed since the start of the contract, not counting 23%. Thus, the longer the insurance policy was used, the lower the final payment amount will be. Some companies provide their own calculator, with which the policyholder can find out in advance the expected amount of payment.

Possible problems when receiving payment

Despite the regulatory regulation of this issue, in practice various difficulties may arise related to receiving funds upon termination of the contract. If the contract does not regulate payment terms in such situations, the organization must transfer the funds within two weeks from the date of receipt of the application. Further deadlines depend on the specific bank, but practice shows that usually the return occurs earlier than the established deadlines.

ATTENTION !!! You should not wait long after the deadline; you should file a complaint with the insurance company as soon as possible. Perhaps the problem arose for internal reasons (accounting entries) and then the company will ask to extend the waiting period, or perhaps the insurer does not plan to pay the funds at all, and therefore ignores the client.

If you receive a refusal or are ignored, you should file a complaint with the RSA, as well as file a statement of claim in court. At this stage, all the documents collected in the previous stages will be important. Judicial practice shows that if all established requirements are met, the claim will be satisfied, but it is important that it be drafted correctly. Disputes with insurance companies have always been complex, so if difficulties arise, it is best to seek legal assistance

In reality, such problematic situations are quite rare. Large insurance organizations protect their reputation and are not ready to lose it for the sake of a couple of thousand in income. This practice is common among small and little-known insurers, which you should be wary of.

The fate of the insurance premium upon termination of the insurance contract at the initiative of the policyholder

Hello colleagues. In the course of my work, a question arose regarding the fate of the insurance premium if the policyholder unilaterally refuses the insurance contract: should the insurance premium always remain with the insurer in such a case?

In paragraph 2, clause 3, art. 958 of the Civil Code of the Russian Federation states that in case of early refusal of the policyholder (beneficiary) from the insurance contract, the insurance premium paid to the insurer is not subject to return, unless otherwise provided by the contract. It is logical to assume that since the insurer has greater bargaining power when concluding an insurance contract (which is especially true for insurance contracts with the participation of consumers), the insurer will not deprive itself of a potential source of profit by establishing in the insurance contract a condition on the return of the insurance premium to the policyholder in the event of his early refusal from the contract.

Bearing in mind this consideration and paragraph 2 of paragraph 3 of Art. 958 of the Civil Code, lawyers most often answer negatively to the question about the possibility of returning the insurance premium to the policyholder if he cancels the insurance contract early. However, in my opinion, this approach to resolving the issue cannot be correct in all cases, in particular, it is, at a minimum, controversial for insurance contracts with the participation of citizen-consumers, and here’s why: 1. In Article 4 of the Federal Law “ On the Protection of Competition" in the definition of financial services, insurance services are directly named as a type of financial services.

2. The preamble of the Russian Law “On the Protection of Consumer Rights” states that a consumer is a citizen who intends to order or purchase, or who orders, purchases or uses goods (work, services) exclusively for personal, family, household and other needs not related to carrying out business activities

3. Article 32 of the Russian Law “On the Protection of Consumer Rights” states that the consumer has the right to refuse to fulfill the contract for the performance of work (rendering services) at any time, subject to payment to the contractor for the expenses actually incurred by him related to the fulfillment of obligations under this contract. Therefore, if we are guided by the principle of lex specialis derogat lex generalis, the consumer has the right to refuse the insurance contract at any time, unless (in the case of concluding a property insurance contract) by the time the consumer is supposed to refuse the contract, the insured property has not been lost (clauses 1, 2 of Article 958 of the Civil Code ), and receive the amount of the insurance premium paid minus the amount of expenses actually incurred by the insurer related to the fulfillment of its obligations under this agreement. This interpretation of the above legislative provisions, in my opinion, is also justified from a political and legal point of view, providing better protection of the rights of the weaker party to the insurance contract - the policyholder-consumer.

What objections, in your opinion, can be made to this approach to resolving this issue?