Today, banks provide many services that are so convenient for modern people to use. These include money transfers, loans, utility bills, and the use of credit cards. The latter can perform many functions, serve to receive a pension, salary, and also use a loan amount provided by the bank. Since almost all calculations are made by computers, it cannot be said that force majeure does not occur in such an institution. Sometimes such equipment simply breaks down or a program crashes in the system. In this case, errors in calculations may be made or some clauses of the contract may be violated. If the client has become a victim of such an oversight, he has the right to write a claim to the bank.

Illegal blocking

Most often, a current account or bank card is blocked when using a plastic card abroad. A little less often, but quite often, the reason for blocking is a strange, from the point of view of Sberbank, transaction within the Russian Federation.

In fact, blocking in some cases is pure arbitrariness of Sberbank, contrary to current legislation.

Yes, Art. 858 of the Civil Code of the Russian Federation states that restriction of the right of a bank client to dispose of their own funds is possible only on the basis of seizure of funds.

Paragraph 2 of Federal Law No. 115 dated August 17, 2001, on the basis of which Sberbank carries out blocking, states that control of client funds can only be carried out in the event of suspicions confirmed by law enforcement agencies about the client’s involvement in extremist or terrorist activities.

Moreover, even if a certain transaction seems suspicious to the bank, due to the requirements of Federal Law-115, it only has the right to refuse to carry out this separate suspicious transaction, but it does not have the right to block the account, since blocking is a restriction of the client’s right to use his own money.

This means that unjustified blockings fall under Art. 10 of the Civil Code of the Russian Federation (abuse of rights) and Art. 285, 330 of the Criminal Code of the Russian Federation.

Help from a lawyer when writing off money from an account

You were illegally debited from your bank card, don’t know where to start? Don't waste time, contact our lawyers who:

- will conduct a thorough analysis of your situation;

- provide advice and explain the provisions of current legislation;

- will offer options for restoring your violated rights;

- will prepare an application, a claim to the bank, a complaint to the prosecutor's office, the Central Bank of the Russian Federation, a lawsuit;

- can represent your interests in relations with the bank, with law enforcement agencies and in court.

What to do if blocked

In case of blocking, most citizens prefer to call the bank, confirm the transaction or provide documents indicating the legality of a particular transfer.

However, not every blocking is without consequences for the bank client. Thus, if the card is blocked, the client may be left in a hopeless situation abroad, be late for a flight, disrupt a business meeting, or not pay for a necessary purchase.

In this case, the client has the right to present a claim to the bank or file a claim in court. Practice shows that the majority of such cases are won by bank clients.

Pre-trial claims under a loan agreement

According to statistics, in most cases, claims are directly related to problems in credit and financial relations with the bank. And this is explained by the fact that the client is convinced that the creditor has violated the terms of the concluded agreement. As practice shows, the most common grounds for filing a pre-trial claim with a banking institution are:

- recalculation of the amount of debt under the contract;

- recalculation of accrued interest in case of early closure of a credit account;

- illegal charging of fines, penalties and other fees;

- refund of funds for insurance services under the contract.

The current legislation of the Russian Federation does not define the obligation to resolve conflict situations in a pre-trial manner. However, in accordance with clause 7, part 2, art. 131 of the Code of Civil Procedure of the Russian Federation, a client’s claim to the bank may become mandatory if the condition for pre-trial resolution of the dispute is clearly stated in the concluded agreement.

Today, resolving disagreements that have arisen between a bank and a client pre-trial is the simplest option for resolving the problem. At the same time, the specifics of consideration of a claim may or may not be provided for by the current contract. The procedure for drawing up and submitting a claim, as well as the timing of its consideration by the bank, will depend on this.

In case of any conflict situations arising within the framework of credit and financial relations, the client should:

- make independent calculations, referring to regulations;

- prepare a succinct but concise text in accordance with the provisions of the contract and current laws;

- attach to the completed application photocopies of documents clearly proving his position.

When drawing up a pre-trial claim regarding a credit relationship, the client must treat it in the same way as preparing a statement of claim in court. The text of the appeal should indicate the intention to go to court if the bank refuses to comply with the requirements or ignores the claim.

Download the claim for early cancellation of credit insurance and return of insurance premium (sample/form)

Download a claim to the bank for refusal of imposed credit insurance (sample/form)

Download the claim for the return of illegal loan fees (sample/form)

Remember that the outcome of the case may depend on the correctness of the claim . If you need help preparing this document, please write about it using the form below.

Other grounds for claims

In addition to disputes over illegal blocking, the reasons for filing a claim with Sberbank may be:

- illegal terms of the loan agreement;

- illegally accrued penalty;

- rudeness or low professional qualities of bank personnel;

- customer problems resulting from failures in banking mechanisms and systems;

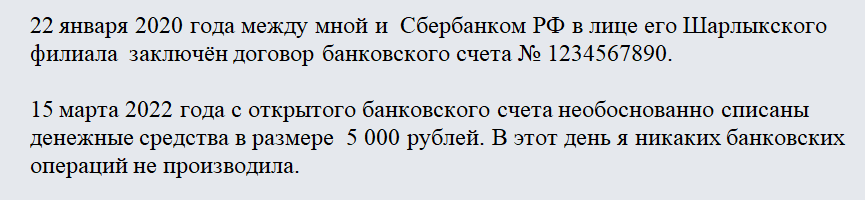

- unauthorized debiting of funds from an account;

- banking spam.

The procedure for writing off money by bailiffs

Unlike the procedure for seizing property, writing off funds from accounts does not require the obligatory presence of the debtor, with the exception of sending a notification to the citizen.

In addition, in order to seize an account and write off money from it, the bailiff is not required to obtain the consent of the debtor.

As for notification, the postal service is responsible for late delivery of a registered letter to the addressee.

The funds are written off after the bailiff performs the following sequential actions provided for by law:

- Initiation of enforcement proceedings on the basis of a writ of execution received by the service;

- Sending an initiation order to the debtor;

- Sending requests to credit institutions for the availability of accounts opened in the name of the debtor;

- Issuance of a resolution on the arrest and write-off of funds in accounts (sent to the bank and the debtor for notification);

- Issuing and sending to the credit institution a resolution to lift the arrest if the written-off funds were sufficient to repay the debt.

Important! If the amount written off was not enough, funds will be written off until the debt is fully repaid.

At the same time, in accordance with the new rules, the bank is not obliged to notify the client about the debiting of funds. Therefore, information about the write-off can only be obtained upon a written request sent to the bank or the territorial division of the FSSP.

How to write a complaint

There is no set form for writing a complaint. This means that it can be written in any form suitable for expressing dissatisfaction. That is why the structure of the complaint is most similar to the complaint known to everyone.

Thus, the claim contains:

- “header”, consisting of the name of the bank to which the claim is sent, and the full name, address and bank details of the author of the claim;

- description of the event that caused dissatisfaction with the bank client;

- requirement to eliminate violations. If the bank's actions, in addition to inconvenience, also caused real material losses, compensation for damage should be demanded.

It is advisable to stock up on information confirming account blocking before submitting a claim. For example, print a bank report on the movement of funds in the account.

You should not base your claims on the basis of the Consumer Protection Law. This law has nothing to do with banks. It will be enough to justify the illegality of blocking through the Civil Code and the Criminal Code of the Russian Federation.

At the end of the text, it is advisable to indicate that the claim was sent in the manner of pre-trial consideration of the dispute. Sberbank is well aware of court practice, and therefore, in the event of its own not entirely legal actions, it will prefer not to bring the dispute to trial.

Sample claim to bank

In the context of resolving disputes between a bank and a client, the claim procedure is a process of pre-trial dispute resolution, within which the client sends a written claim (statement, complaint) to the bank outlining the essence of the dispute and its requirements, in response to which the bank makes a decision within a specified period of time , which also notifies the client in writing.

From the point of view of controversial situations concerning monetary issues and demands, as a rule, a claim (rather than a complaint) is always sent to the bank, less often a statement, and then only on condition that this form of resolution of monetary disputes is provided for by the terms of the agreement with the bank.

Compliance with the claim procedure may be optional (optional) or, on the contrary, mandatory. In the latter case, failure to comply with the claim procedure becomes a barrier to going to court. From the point of view of legal relations between the bank and the client, the mandatory pre-trial settlement of the dispute may be provided for in the contract. At the same time, simply including such a condition in a contract does not mean a legal obligation to fulfill it.

The claim procedure must be clearly, specifically and in detail, defining in particular the form of the claim, the grounds for filing it (at least in general terms), the timing and procedure for filing and considering the claim.

Detailing the terms of the claim procedure in the contract does not limit the client on the grounds for filing a claim. In principle, you can contact us regarding any violation of your rights and interests, which, by the way, clients often do. Moreover, clients often use the claim procedure, even if it is not provided for in the contract, as a simpler, more convenient and faster way to resolve a problematic situation than a tedious and costly trial.

After receiving a claim, the bank is obliged to:

- Consider the appeal and requirements.

- Make a decision on the claim.

- Notify the client within the prescribed period of the decision made.

The deadlines for filing and consideration of claims are usually established by an agreement between the bank and the client. In this case, banks are guided by internal bank rules and regulations, so the terms may vary depending on the bank, the content of the legal relationship and the basis for the application.

- Internal documents (regulations, regulations) of the bank on the procedure for filing and considering claims. Typically, the established deadlines, depending on the type of service, the basis and method of filing the claim, range from 1 to 30 days, rarely - up to 60 or more days.

- The law to which the current situation falls. The legislation does not provide for a universal period. Often, clients are guided by the 10-day period established by the Consumer Protection Law, which is not always correct, since this law covers only some cases of the provision of financial services and related claims. The general rule on the claims procedure for resolving disputes provides for a “reasonable period”, in other words, the sooner the better. In practice, no more than a 30-day period for consideration of claims is often used, which is well within the standard deadlines established by most Russian banks.

When determining the deadlines for banks to consider claims, it is important to understand:

- the mandatory nature of the claim procedure can be such only due to the presence of this condition in the contract, which means that the client, by signing the contract, agrees with the procedure and terms that apply in the bank;

- the claim procedure, applied optionally, does not impose strict time limits on the bank - as a rule, they are guided by their internal rules.

A reasonable period for banks to consider a claim is 10-30 days. This is confirmed by the position of the courts.

There is no strict form for writing a claim to the bank, just as there are no serious restrictions on the methods of sending it. As a rule, claims are accepted directly at the bank, by mail, through the feedback form on the website, e-mail, and other communication channels. Any method of submitting a claim is beneficial for the client, which allows the bank to record the fact that it has been received by the bank.

To prepare a claim, you can use numerous samples presented on the Internet and on our website. If such a possibility exists, it is worth turning to the samples that are available on the bank’s website or in its branches.

- The name of the bank and the person to whom the claim is addressed. Typically, the claim is sent to the head of the bank or branch where the client is served.

- Client’s personal data (full name, contacts).

- Document title: “Claim”.

- The main part is a description of the factual circumstances of the case, violations of rights and interests. When preparing the text, it is important to observe chronology, logical sequence, write briefly, with an emphasis on the most important details, not forgetting about the specifics - dates, times, events, bank employee data, etc.

- Arguments and arguments in favor of your position with references to the law, contract provisions and available evidence, for example, payment documents. It is advisable to attach all the evidence indicated in the text to the claim in the form of copies.

- Specific requirements for the bank.

- A request to consider the claim within a certain period (10-30 days) from the date of its receipt.

- Desirable method of receiving a response to the claim and address. It is advisable to indicate a telephone number for contacts.

- Date of preparation, personal signature.

If there are problems with preparing a claim, or it is extremely important to draw up an impeccably competent document, including in legal terms, it is worth using the help of a lawyer. You can leave your request in the pop-up form in the lower corner of the screen.

According to statistics, the majority of monetary claims are related to credit legal relations and their derivatives. This is understandable both due to the serious volume of the lending market and the often arising conflict of interests. Unfortunately, imperfections in the legislative framework, economic instability, tricks and violations of the law on the part of the banking sector often manifest themselves to the detriment of the interests of clients.

Within the framework of credit legal relations, the most frequently filed claims are:

- on recalculation of debt under a loan agreement;

- on recalculation of interest upon early repayment of the loan;

- about the return of insurance.

In order to resolve the above issues, almost all banks provide for the client to submit appropriate applications in the form established by the credit institution. Claims are sent directly either in the event of a dispute or in situations where the bank has not responded to the client’s application or made a decision that violates his rights.

The requirement to recalculate debt may be due to various circumstances:

- early partial repayment;

- unlawful accrual of commissions, penalties, penalties;

- incorrectly (erroneously or intentionally) performed previous recalculation;

- the client wishes to return, in his opinion, the excessive amount paid to repay the debt.

A claim for recalculation of interest upon early repayment of a loan is sent to the bank in the following cases:

- if the recalculation for partial repayment of the loan was not made automatically;

- the bank did not fulfill the client’s request for recalculation of interest, indicated by him in the statement of intention to repay the loan early;

- the bank made an error in the calculations;

- if a request is made to recalculate interest on a repaid loan and return the overpaid amount.

We suggest you familiarize yourself with: Inheritance after the death of a husband, rights of inheritance by law after the death of a spouse, how the inheritance is divided, how to register, how to enter into the inheritance, what is the wife’s share

Insurance claims are a common practice. If the bank acted as a beneficiary, it is not interested in the return, and, more importantly, it almost never does this on its own initiative. Here, a claim, in fact, is the only opportunity, firstly, to state your demands, and secondly, to find out the bank’s position. There are also few options for pre-trial resolution of the dispute - either the bank will return the overpayment for insurance, or you will have to go to court.

In any dispute over loans, it is very important:

- prepare your calculations and it is best if this is done by a specialist who can simultaneously indicate calculation formulas and links to regulations;

- present your position in a reasoned and convincing manner, citing the provisions of the laws;

- Attach to the claim copies of contracts, payment documents and correspondence with the bank, if it previously took place.

When preparing a claim for a loan, you should treat it in the same way as if you were preparing a claim in court. In the claim itself, it is advisable to indicate your intention in the future, in the event of the bank’s refusal to fulfill the requirements, to seek judicial protection.

In the upper right corner of the application, indicate the recipient's details: full name, position, address of the main bank office. Then indicate who is making the claim. Remember that on paper you need to indicate your full name only in the genitive case (you are answering the question “from whom the claim is being sent”). Indicate the phone number and address of the sender. There is no period at the end of this entry.

Indent a line and write the word “claim” in capital letters in the middle of the sheet. Then state the requirements for the bank in free form.

Claims are considered by the bank in accordance with internal regulations. A bank employee will inform you about the time frame for receiving a response. Make sure that managers register the application and assign it an incoming number.

If the bank violates the terms of the loan agreement, do not rush to go to court. This is a costly process that will take two to three months. First, make a written claim to the bank in pre-trial order. In your complaint, indicate the clauses of the loan agreement that the bank violated. If necessary, request a recalculation of the interest rate or termination of the contract.

How to send

There are two generally accepted methods of serving a claim:

- personally or through a proxy;

- by mail.

It is these two methods that make it possible to confirm the fact of delivery of the claim.

For this purpose, upon personal delivery, a bank employee must be required to sign for receipt and affix the appropriate stamp. If the mailing method is chosen, the claim must be sent by registered mail with return receipt requested.

You can also submit a claim directly on the Sberbank of the Russian Federation website if receiving confirmation of shipment is not important.

If, instead of a addressed complaint, the client decides to write a complaint against the bank, then it can be sent:

- to Rospotrebnadzor, which has the right to inspect banking activities based on applications from bank clients;

- in the Central Bank of the Russian Federation, which controls all banks operating on the territory of the Russian Federation. Intervention by the Central Bank can be effective in the event of credit disputes with Sberbank;

- to the Prosecutor's Office regarding any actions of Sberbank;

- to the Federal Antimonopoly Service. It is recommended to contact this authority in case of dishonest advertising by Sberbank that is silent on certain terms of the loan agreement.

Credit relations

Most often, a claim to a bank contains requests that include:

- recalculation of loan amounts, including early repayments;

- revision of the interest rate or its recalculation, most often when refinancing or restructuring a loan, as well as during early payments;

- refusal to participate in insurance programs;

- return of illegally written off amounts (fines, penalties, commissions, erroneous deductions).

It is advisable to support any claim with your own calculations, correctly stated and carried out on the basis of the information specified in the contract. Under no circumstances act on your own, ignoring bank requirements. You cannot repay only that part of the debt that you consider legal, because the bank accepts performance obligations in accordance with Art. 5 p.

- Interest-bearing debt.

- Debt on the principal part of the debt.

- Penalties.

- Interest accruals in the current period.

- Part of the principal debt for the current period.

- Other legal payments.

In the case of refusal of insurance, the application is a necessary measure, since the bank itself never initiates such a return. The response to any claim will make it possible to find out the position of the creditor, and if you disagree with it, you can contact the judicial authorities or the Central Bank of the Russian Federation.